Energy should be free, or at the very least, cheap. It’s a basic necessity for modern living, after all. But, alas, we lose our hard-earned money every month to power companies who keep raising their prices.

An effective way to counter this is to own a solar system that generates free energy – but that, too, takes thousands of dollars. Lucky for you, though, there are ways to soften the blow. 6 of them, in fact.

What are these, you ask? None other than solar financing.

Listed below are your options. I recommend you read them from top to bottom but feel free to click on any of the bullets to skip sections.

- Personal loans

- Green loans

- Adding solar to your home’s mortgage

- Solar leasing

- Power Purchase Agreements (PPA)

- Interest-free loans

1. Personal loans: Cheaper solar panels, higher interest rate

Personal loans are going to be most people’s first borrowing option. Probably yours, too – and for good reason.

As long as you have good credit, getting a personal loan approved by a lender should be easy. Moreover, compared to green loans and other options, the process of getting a personal loan is more straightforward.

Then, when you have the loaned cash with you, you’re going to have the same buying power as someone who pays with his own money. This is a crucial point since the cost of installing solar panels is generally cheaper if you pay cash upfront because it gives you more leverage to negotiate.

The downside is that, again, you likely need good credit before you get the loan approved. Additionally, personal loans tend to have higher interest rates than some of your other finance options on this list.

Get 3 Solar Quotes From Quality Local Installers.

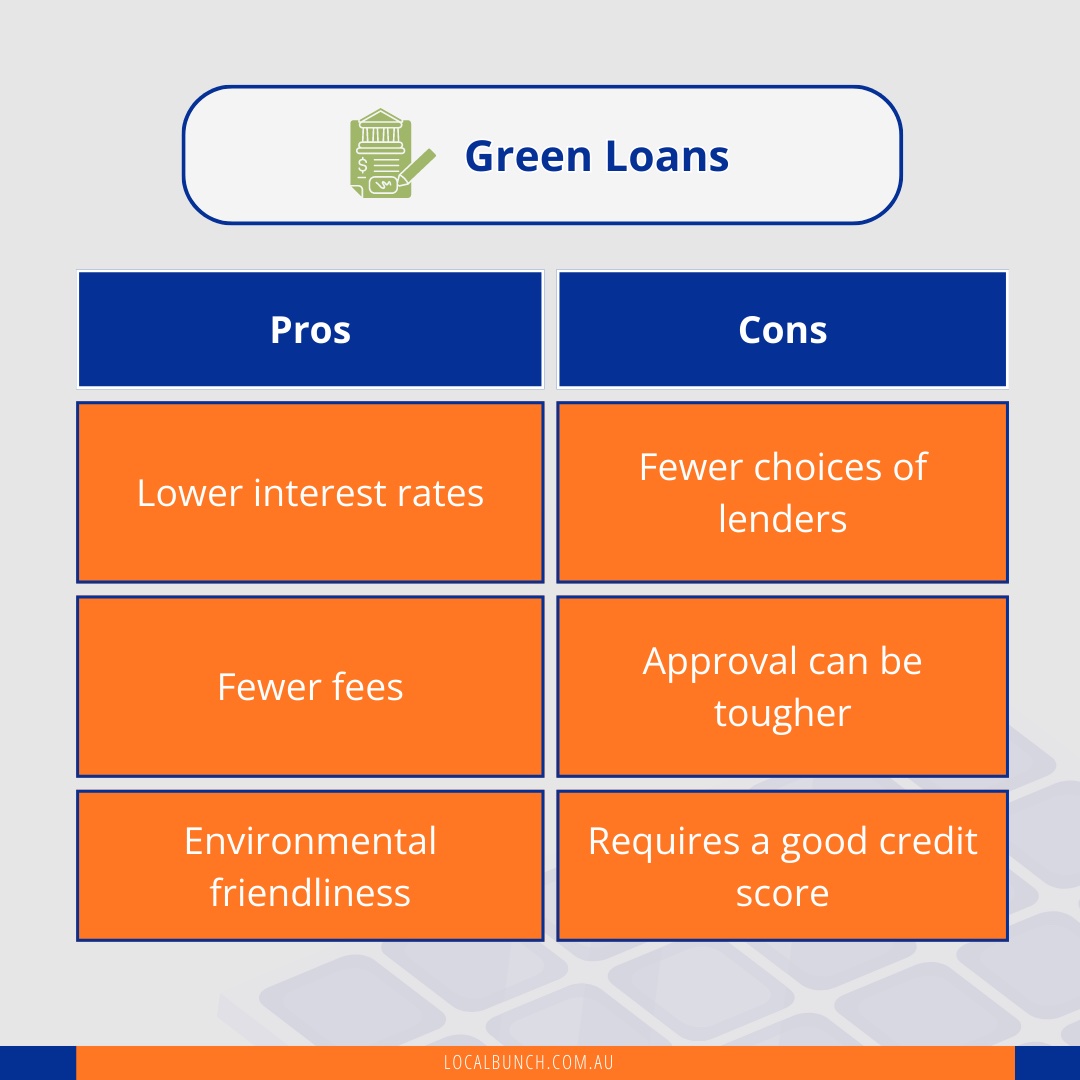

2. Green Loans: Environmentally friendly, more challenging approval

Green loans are much like personal loans. What makes them unique, however, is they’re a financing option provided by lenders who loan you money to buy environmentally-friendly products, including solar panels.

To be honest, though, there aren’t many financial institutions that can offer you a green loan.

Despite that, this type of loan should still be a priority if you can get it because it has fewer fees and lower interest rates. Consequently, this shortens your solar payback period, giving you access to free energy that much faster.

Other drawbacks you need to be aware of include a more challenging approval process and, similar to a personal loan, a good credit score.

3. Adding solar to your home’s mortgage: Low-interest rate, more debt

As of today, the interest rate, if you add the cost of your solar panels to your home’s mortgage payment, is quite low. Add that to the savings you’re going to get from your solar system and this makes it an incredibly attractive financing option right now.

The downside, of course, is that you’re adding to your debt since mortgage is, technically, still debt (albeit a good one). And because it’s debt, the longer you take to pay it, the larger the totality becomes.

That being said, lower energy bills can more than offset your bloated mortgage if you play your cards right.

So, before you decide, I recommend you take the time to carefully plan your finances. Furthermore, compare the total amount of money you’re going to spend if you add your solar system to your mortgage versus if you engage with your other loan options.

4. Solar leasing: No upfront cost with snide interest rates

Let me start you off with why you should consider solar leasing.

For one, you don’t have to shell out any money to have solar panels installed in your home. Second, because you didn’t pay anything upfront and you get lower power bills right away, you also save money immediately.

That’s amazing, right?

Well, like the other solar loans listed here, there are drawbacks.

First, it’s a lease. So you technically don’t own the solar system until after you’ve paid it in full.

Moreover, don’t be fooled by the supposedly low-interest rate. In most cases, prices of solar systems have already been marked up before applying interest. So, in the end, the total cost tends to be higher which, in turn, brings down the sum of your savings.

Get 3 Solar Quotes From Quality Local Installers.

5. Power Purchase Agreement (PPA): You pay significantly less for power

With power purchase agreements or PPA, a solar retailer will install a solar system on your roof at no cost to you. No upfront costs and you don’t have to pay for the solar panels either.

The catch is that you don’t actually own the solar panels on your roof. The retailer does.

Moreover, by agreeing to have their solar panels on your home, you’re also agreeing to buy the solar power it generates. There’s usually a minimum amount you have to buy, too.

What makes this better than buying energy from the grid, however, is that they sell power at a significantly lower price. So, even if you technically don’t own a solar system, you still get to enjoy the benefits of having one. At least to a certain degree.

That being said, I recommend PPA only if you use most of your power during the day. Why? Because solar panels only generate energy during the daytime and you must take advantage of that due to the required minimum you have to buy.

6. Interest-free loans: The most shady option around

Like the last couple of options, interest-free loans are also marketed as having no upfront costs and, well… 0% interest rate. Other descriptions you might hear from salesmen include straight monthly repayments, buy now pay later, and other things of that nature.

Getting approved for this loan is also much, much easier even if you don’t have good credit. This makes it accessible to a wider group of people.

Sounds too good to be true, doesn’t it? That’s because it is.

The quote you’re going to get is already marked up significantly more than usual to cover the supposedly non-existing interest. Some markups even go as high as 25%, if not more. Quite shady if you ask me.

I would only recommend this after you’ve exhausted all your other options.

Conclusion

All things equal, a green loan is the best solar finance option you have in Australia. Firstly, it has low interest so you keep more of your money in your pocket. Secondly, you get to have a more positive impact on the environment.

However, not everyone can get approved for a green loan. Therefore, the right financing option for your solar system ultimately depends on your personal circumstances.

Check your financial situation, your energy consumption and habits, as well as your long-term plans to see which of the 6 options works best for you. Then, when you’re ready, come back to us so we can help.

We have a network of pre-vetted installers that we trust with our own systems and money. You can trust them, too. Let us know if you need our help and we’ll get you 3 FREE quotes right away.